I love days like today. ASX indexes are down over 2% and fear is entering the market. My sale of NAB at $36 or $37 including options premium looks like great with NAB trading down today to $34. I will continue to stay on the sidelines for great opportunities to present, just like it did when NAB was trading under $30.

Keep powder dry and wait for bargains to appear.

Wednesday, June 07, 2006

Wednesday, April 05, 2006

Figuring out trading range

Posted by Bakuv http://boards.fool.com/Message.asp?mid=23934359&recscode=2

Ok, since I can be dense sometimes, mind if I restate the trading range methodology using USANA as an example?

1) Record the ttm EPS for the 3Q: $1.90

2) Record the low and high trading prices following the release of 3Q results until the 4Q results are released: $37.30 and $47.36

3) Establish PE range for the trading range following the known EPS: 19.63 (=37.20/1.90) to 24.92 (=47.36/1.90)

4) Record the ttm EPS for the 4Q: $1.98

5) Apply previous PE range from step 3 to just released 4Q ttm EPS of 1.98 to get new trading range until next quarter's results are announced: 38.87 (=19.63*1.98) to $49.34 (=24.92*1.98) (btw, I came up with a different low end of the trading range, 38.87 instead of 38.26)

6) Can throw out extreme low and high prices based on common sense and use prices that are more realistic

7) Record events that cause price fluctuation in order to "price" news.

8) Rinse and repeat each quarter

Ok, since I can be dense sometimes, mind if I restate the trading range methodology using USANA as an example?

1) Record the ttm EPS for the 3Q: $1.90

2) Record the low and high trading prices following the release of 3Q results until the 4Q results are released: $37.30 and $47.36

3) Establish PE range for the trading range following the known EPS: 19.63 (=37.20/1.90) to 24.92 (=47.36/1.90)

4) Record the ttm EPS for the 4Q: $1.98

5) Apply previous PE range from step 3 to just released 4Q ttm EPS of 1.98 to get new trading range until next quarter's results are announced: 38.87 (=19.63*1.98) to $49.34 (=24.92*1.98) (btw, I came up with a different low end of the trading range, 38.87 instead of 38.26)

6) Can throw out extreme low and high prices based on common sense and use prices that are more realistic

7) Record events that cause price fluctuation in order to "price" news.

8) Rinse and repeat each quarter

Tuesday, April 04, 2006

CTRP fears

Orignally posted on CTRP board at Fool SA. http://boards.fool.com/Message.asp?mid=23931220

Just came here on the trail of nikita02445 who had a board created, named and posted to by her.

"PS - I know this is probably a stupid question, but when is there first quarter?"

First quarter is generally Jan-Mar each year, with lots of exceptions. Individual companies can have first quarter when ever they want, so some might be giving their third quarter numbers during the first quarter!! Some countries have different first quarters where companies must align with Fedral tax laws, exceptions are such a drag, why can't we just have rules!! Did you know that some things that many Americans think of as the rule or the norm is from a global perspective the exception. Metrics rule. Just think how hard all this stock investing would be if it was still in fractions!!

Great post on pandemic nikita. TysonL any chance of paragraph or two summing up False Alarm: The Truth About the Epidemic of Fear.? My partner is a Biotech project manager and is doing a Masters in Drug Development. She is the least easily influenced person I know and has an excellent mind. As she doesn't have any vested interest, her opinion is valuable to me. Almost everyone that has a loud voice in a massive topic like pandemics have vested interests, they are on one side.

Her view is, there will be lots of warning sign of the pandemic coming; first the virus needs to mutate to allow consistent human to human transmission. When that mutation happens you will still have a lot of time to prepare. Gee I must really pin her down on what a lot of time is, words like “a lot” are so meaningless due to their subjectivity. Avian flu is being so closely monitored that we will see the signs early. A pandemic will happen sometime.

My view is that it can't hurt to have some extra toilet paper, canned and dry goods lying around and hopefully you have a veggie garden, maybe some solar power, some water tanks (essential in Australia) a holiday home in some remote location, bottled gas and bbq, lots of guns (joking, though it really scares me that depending on the source somewhere around 32-39% of households contain at least one firearm), a stash of gold coins and many other things. It can't hurt unless you put all of that on credit card. Hopefully y'all know you shouldn't get in bad debt (debt that costs you), even if that's what your leaders consistently do.

I once read that at it's peak 50,000 people died a year on American roads. Imagine if the government and vested interest groups pushed that information as propaganda to create fear amongst motorists. Would you be more afraid to drive?

I also read that human's perception is strongly influence by recent events; we haven't had an epidemic since Spain hence we think it is unlikely to happen.

The evil pharmaceutical companies (I'm joking, my partner hates that phrase. Why is an entire industry so maligned 'cos a few bad practices amongst a few companies?)and there are several, Tamiflu is but one, will pump like never before.

Tired, should be sleeping eating anything but this. Hope that made some sense. I say act quickly when the signs are there, but do not live you life in fear. This is America's time, your window is closing, you can have a beautiful renaissance, you can make the coming century one to be rejoiced like the Italian Renaissance of the 15th century. http://en.wikipedia.org/wiki/The_Renaissance

Nikita, if you are still reading, your board on Gems is making a lot of people happy. I am one of them. If you have indeed left the hidden gems fold I hope they have arranged for you to at least read your board, or better have listened to your request for deeply discounted third, fourth etc subscriptions.

Nikita I am sure you know this, but did everyone already see this irony? http://www.ctrp.org/

PPS I am a paranoid guy who talks and writes as a way to think, so any view that I ever express is often not my strongest view, hope my off-track comments don't offend anyone, well really I hope that the level of fear in your country hasn't progressed so far that anyone could view this with a devil's light. I don't even know what a devil's light is.

Dean

Just came here on the trail of nikita02445 who had a board created, named and posted to by her.

"PS - I know this is probably a stupid question, but when is there first quarter?"

First quarter is generally Jan-Mar each year, with lots of exceptions. Individual companies can have first quarter when ever they want, so some might be giving their third quarter numbers during the first quarter!! Some countries have different first quarters where companies must align with Fedral tax laws, exceptions are such a drag, why can't we just have rules!! Did you know that some things that many Americans think of as the rule or the norm is from a global perspective the exception. Metrics rule. Just think how hard all this stock investing would be if it was still in fractions!!

Great post on pandemic nikita. TysonL any chance of paragraph or two summing up False Alarm: The Truth About the Epidemic of Fear.? My partner is a Biotech project manager and is doing a Masters in Drug Development. She is the least easily influenced person I know and has an excellent mind. As she doesn't have any vested interest, her opinion is valuable to me. Almost everyone that has a loud voice in a massive topic like pandemics have vested interests, they are on one side.

Her view is, there will be lots of warning sign of the pandemic coming; first the virus needs to mutate to allow consistent human to human transmission. When that mutation happens you will still have a lot of time to prepare. Gee I must really pin her down on what a lot of time is, words like “a lot” are so meaningless due to their subjectivity. Avian flu is being so closely monitored that we will see the signs early. A pandemic will happen sometime.

My view is that it can't hurt to have some extra toilet paper, canned and dry goods lying around and hopefully you have a veggie garden, maybe some solar power, some water tanks (essential in Australia) a holiday home in some remote location, bottled gas and bbq, lots of guns (joking, though it really scares me that depending on the source somewhere around 32-39% of households contain at least one firearm), a stash of gold coins and many other things. It can't hurt unless you put all of that on credit card. Hopefully y'all know you shouldn't get in bad debt (debt that costs you), even if that's what your leaders consistently do.

I once read that at it's peak 50,000 people died a year on American roads. Imagine if the government and vested interest groups pushed that information as propaganda to create fear amongst motorists. Would you be more afraid to drive?

I also read that human's perception is strongly influence by recent events; we haven't had an epidemic since Spain hence we think it is unlikely to happen.

The evil pharmaceutical companies (I'm joking, my partner hates that phrase. Why is an entire industry so maligned 'cos a few bad practices amongst a few companies?)and there are several, Tamiflu is but one, will pump like never before.

Tired, should be sleeping eating anything but this. Hope that made some sense. I say act quickly when the signs are there, but do not live you life in fear. This is America's time, your window is closing, you can have a beautiful renaissance, you can make the coming century one to be rejoiced like the Italian Renaissance of the 15th century. http://en.wikipedia.org/wiki/The_Renaissance

Nikita, if you are still reading, your board on Gems is making a lot of people happy. I am one of them. If you have indeed left the hidden gems fold I hope they have arranged for you to at least read your board, or better have listened to your request for deeply discounted third, fourth etc subscriptions.

Nikita I am sure you know this, but did everyone already see this irony? http://www.ctrp.org/

PPS I am a paranoid guy who talks and writes as a way to think, so any view that I ever express is often not my strongest view, hope my off-track comments don't offend anyone, well really I hope that the level of fear in your country hasn't progressed so far that anyone could view this with a devil's light. I don't even know what a devil's light is.

Dean

Saturday, March 04, 2006

AKAM thought

Posted http://boards.fool.com/Message.asp?mid=23790238&post=true

In case anyone wants to follow the Street's advice, why not get paid to do so.

April 25 Put options closed at .90 3 March

http://au.finance.yahoo.com/q/op?s=AKAM&m=2006-04

Trading costs aside that gives you $90 to place a limit order for every 100 shares you want to buy, e.g. 400 shares, you get $360 to wait.

- If AKAM keeps going up you get to pocket $360 and sell put the next month.

- If it goes down you have same risk as having bought the stock, except your cost is 24.10 (25-.9) instead of current 26.10.

- If it stays the same you pocket the $360.

Surely paying the right price is one of the main rules of successful investing and to me it appears like the analyst is simply trying to do that, buy at the right price.

I think AKAM is a great company and am currently long with Calls sold on 2/3 of position.

I may be way off track but has greed made you think the only direction AKAM can take is up? It might keep going up, but at some time it will have a fall, and it is then that I will be happy to buy more if the story is the same as now.

Update on NAB Call

March 36 NAB calls were sold for .65, as per post on Super Fund if these are called then Super Fund will sell April 36 or 37 NAB put. The funds form the Trust's share sale will be used to pay off the Trusts margin loan. The trust will wait for favourable purchases, with the assurance that it can call on the loan when any opportunity arises.

Friday, February 24, 2006

Short, but what variety.

Short, but what variety.

The markets are fully congested and ready for a big move. We believe this the move is going to be a strong down move and will position accordingly. There are lots of options to do this:

Sell Calls

Buy Puts

Combination of the above

The markets are fully congested and ready for a big move. We believe this the move is going to be a strong down move and will position accordingly. There are lots of options to do this:

Sell Calls

Buy Puts

Combination of the above

Thursday, February 16, 2006

Fool AKAM post

http://boards.fool.com/Message.asp?mid=23716775

Hi Tim

Firstly, thanks for the fantastic analysis and continued thought on Akami.

After your initial recommendation, I quickly jumped on board for the following reasons.

- High fixed costs business with expanding sales, resulting in expanding profitability, i.e. more of there sales fall straight to the bottom line.

- Although there are some competitive risks, I saw and still see 2006 as the first breakout year for web downloads, on the road to downloads that will dwarf those of today. There needs to be some

So I saw a company in the sweet spot, a spot that should get sweeter over the next year or two. With this P/E should expand as more coverage and enthusiasm builds, so expanding earnings with rising P/E multiple can only mean big price increases.

So where are we now,

EPS TTM .52

Price 02-16-06 26.67

P/E TTM 51

EPS high est 06 0.71 ( a 36% increase)

P/E forward 37.6

EPS high est 07 0.94 ( year on year 32% increase)

P/E forward 2 28.37

Looking at this makes me think a few things:

- Are analyst’s estimates too low? With AKAM expanding sales and margin could they blow these numbers away? Maybe.

- If they meet estimates then in two years at today’s price they would still have a P/E of 28. As they had been growing at 30%+ for a number of years they may be rewarded with a higher P/E, lets say 40, putting price around $37.

- What happens if they have one missed estimate, Google starts to move in, Apple gives them the flick or general market conditions deteriorate? P/E will compress as investors enthusiasm wanes, lets say it comes down to TTM P/E of 30. That would take the price back to $16, using forward eps of .71 price would be $21.

Other thought:

- I agree with Tim Hart, Google will start finding things harder. They don’t have trust. Heck I don’t trust them, even though I use their sites everyday. So why don’t I trust them? Probably, as in desperation their competitors have started spreading rumours and innuendoes about their motives. I have no real reason to distrust them, but just like Microsoft I do. Is big bad?

Disclosure: I own AKAM and recently traded Feb 25 Calls for a profit of .50. I am now looking at August Calls.

Wednesday, February 15, 2006

Roll CRYP or be called

CRYP Feb 20 Call.

The story here is different than AKAM, as it will definitely be called in 2 days and we will still own 300 shares. CRYP has had an excellent run from its lows to current 23.59 USD 1.27 (5.69%)

1.27 (5.69%)

The story here is different than AKAM, as it will definitely be called in 2 days and we will still own 300 shares. CRYP has had an excellent run from its lows to current 23.59 USD

- Dividend coming due. US$0.07 per common share. The dividend will be paid on March 15, 2006 to shareholders of record as at March 8, 2006. The ex-dividend date will be March 6, 2006

- Looks like can only get .1 - .4 credit. Even at .4 and with dividend covering trading costs, it is only a 2% return for risk of holding.

Should I roll that AKAM Call

AKAM Feb 25 Call expires in 3 days, should I roll it as current 25.10.

If share neutral then made 21% annual return.

If share falls can buy back option for cheaper and sell share, so limits downside risk.

Down side little participation in upside, need to investigate further to decide on upside potential.

The figures are:

Yes AKAM is a cash machine with digital delivery. Digitial delivery is gonna explode, but Google is about to pounce and all it takes is one hiccup for price to slide.

Sell AUG Call, look to sell March Put.

- May or may not be called, but I want to make decision, not let market make it.

- Capital Gains, when did I buy? 27/07/2005 so to far, but should consider Aug Calls, to see.

- Is call for entire holding, ie will I still profit in any further upside? Yes entire 500.

- Mar Call credit - .80. or $385 Net, for 30 days on $25 OR 3.2%, annual 38%

- May Call credit - 1.85, 93 days, 7.4%, annual 29%

- Aug Call credit - 2.7, 184 days, 10.8%, annual 21%

If share neutral then made 21% annual return.

If share falls can buy back option for cheaper and sell share, so limits downside risk.

Down side little participation in upside, need to investigate further to decide on upside potential.

The figures are:

| P/E (TTM) | 48.88 | P/Sales | 13.38 | |

| P/E (Forward) | 35.31 | P/Cash Flow | 45.73 | |

| Earnings/Share (EPS) | 2.2 | Book Value/Share | 4.11 | |

| PEG | 1.35 | P/Book | 6.07 | |

| Debt/Equity | 0.32 | Cash Flow/Share | 0.55 | |

Yes AKAM is a cash machine with digital delivery. Digitial delivery is gonna explode, but Google is about to pounce and all it takes is one hiccup for price to slide.

Sell AUG Call, look to sell March Put.

Monday, February 13, 2006

Sitting Tight

Hold Telstra and NAB. Stories are improving at both. Sell NAB calls if good oportunity.

Friday, February 03, 2006

Confused? I am...but holding steady

The trust's US account continues to outperform the main US indexes. The account in now about 18% in cash and has a short term aim of 25% cash until the picture clears in the US. Despite the large cash holding the trust has still been outperforming during up weeks. The main reason for this is superior stock selection based on Motley Fool recommendations combined with option trading to generate income for the account.

David Nicholls projects a weekly close below 1261 will move markets in to secular bear with a 25% drop in to 4 year low in October 06. Well 950 on S&P would be scary, if this does occur the trust will be big buyers at that point. The cash holding has been built up with this downside risk in mind. As we are still invested 80% we will profit if market continues higher.

On the positive side Stealth Stocks Dennis Slowether (sp?) and McMillan are pointing for an up year. Analysts are pointing to International stocks heading higher and US stocks lagging.

The trust is happy with their current positioning and looks to decrease holding on further rises.

David Nicholls projects a weekly close below 1261 will move markets in to secular bear with a 25% drop in to 4 year low in October 06. Well 950 on S&P would be scary, if this does occur the trust will be big buyers at that point. The cash holding has been built up with this downside risk in mind. As we are still invested 80% we will profit if market continues higher.

On the positive side Stealth Stocks Dennis Slowether (sp?) and McMillan are pointing for an up year. Analysts are pointing to International stocks heading higher and US stocks lagging.

The trust is happy with their current positioning and looks to decrease holding on further rises.

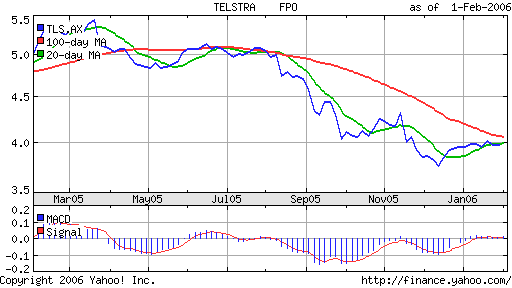

Thursday, February 02, 2006

Holding Telstra

The Trust will continue to hold Telstra. The latest pop in share price on news of T3 in encouraging that the trustees original investment thesis will be fulfilled. The trust will be able to sell some of it's holding over the average paid and will have netted the attractive dividends for that period. Despite being in the troubled Telecommunications industry the trustees had believed if as the largest shareholder the government had known any information that would have led them to believe $5.25 for not a realistic price for T3 then they would have stated that and lowered their price accordingly. However, despite having the knowledge they did not lower their price target. This resulted in the Trusts purchase of a volume and portfolio percentage of the shares far greater than they would normally allocate to an individual share. The other contributing factor was the announcement of the special dividend combining to form $.40 a year in franked dividend. Was that a bribe to unload shares by the company?

At any rate the dividend has been better than interest and as stated the trustees believe they will get to sell above the average price, some time in the future. They will look at call options on Telstra.

Near term technical positive developments would be 20 day cross 100 day, MACD rise above zero, ie share price go up.

Fundamental improvements looked for : Positive wireless and broadband trends, T3, dividend maintained, upside earnings.

At any rate the dividend has been better than interest and as stated the trustees believe they will get to sell above the average price, some time in the future. They will look at call options on Telstra.

Near term technical positive developments would be 20 day cross 100 day, MACD rise above zero, ie share price go up.

Fundamental improvements looked for : Positive wireless and broadband trends, T3, dividend maintained, upside earnings.

A Saucerful of Secrets

A Saucerful of Secrets is not a technical analysis term, it's not the new pot and handle formation. It is the name of one of the best Pink Floyd albums either, one of the two PF albums on which Syd Barrett wove his twisted genius. The album reminds me of the markets in many ways, it takes many twists and turns and the market is most certainly a saucerful of secrets.

With NAB rising steadily off its $26 low 117 months ago to trade above $34.50 now is a good move. Along with three dividends totaling $2.49 plus franking credits, it has been a good investment.

The trust does intend to have numerous banking and investment holding over the years and does plan to hold these shares for a number of years. However, covered call options will be written when the trustees believe the shares have risen close to a short term high. Puts will be written to purchase stocks. Transactions will be executed based on some or all of the following considerations; technical and fundamental analysis, portfolio, tax and income.

Based on the belief that NAB is close to a near term high and it's shares will be able to be purchased for around current values within the next year the trustees will look at possible options priced at 35. As the MACD is rising the trustees are happy to to look for an entry over the coming weeks.

With NAB rising steadily off its $26 low 117 months ago to trade above $34.50 now is a good move. Along with three dividends totaling $2.49 plus franking credits, it has been a good investment.

The trust does intend to have numerous banking and investment holding over the years and does plan to hold these shares for a number of years. However, covered call options will be written when the trustees believe the shares have risen close to a short term high. Puts will be written to purchase stocks. Transactions will be executed based on some or all of the following considerations; technical and fundamental analysis, portfolio, tax and income.

Based on the belief that NAB is close to a near term high and it's shares will be able to be purchased for around current values within the next year the trustees will look at possible options priced at 35. As the MACD is rising the trustees are happy to to look for an entry over the coming weeks.

Saturday, January 21, 2006

Pat on the back

The call made back in October was extremely accurate and profitable.

The trusts performace for the year was 5.68% comapred to 1.24 for the cubes and 3.01 for the spiders.

The trusts performace for the year was 5.68% comapred to 1.24 for the cubes and 3.01 for the spiders.

Subscribe to:

Comments (Atom)